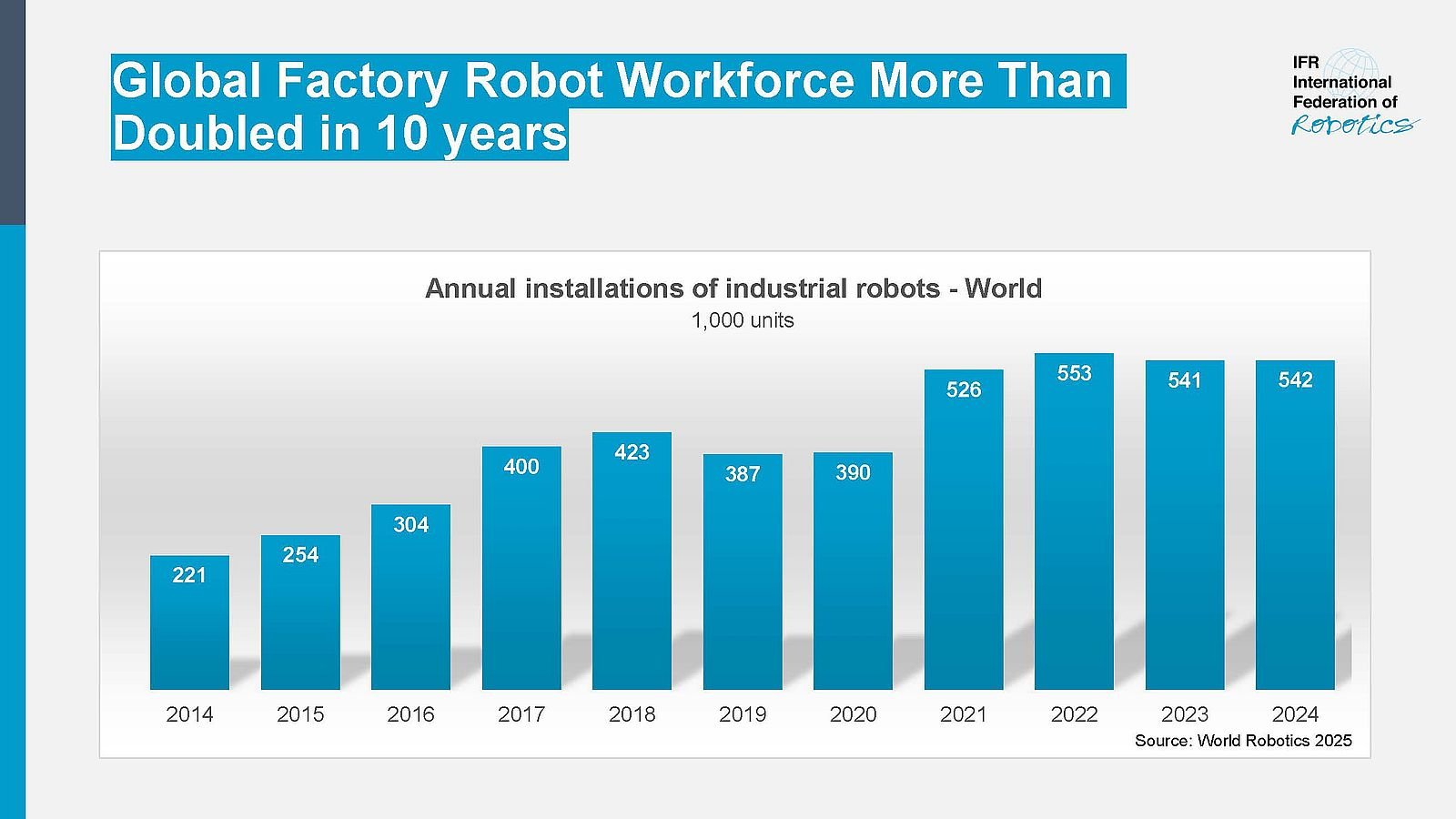

The “World Robotics 2025” report by IFR (International Federation of Robotics) showed that 542,000 industrial robots were installed in 2024 globally. This is more than double the number 10 years ago. Annual installations topped 500,000 units for the fourth straight year. Asia accounted for 74% of new deployments in 2024, compared with 16% in Europe and 9% in the Americas.

China is the largest market

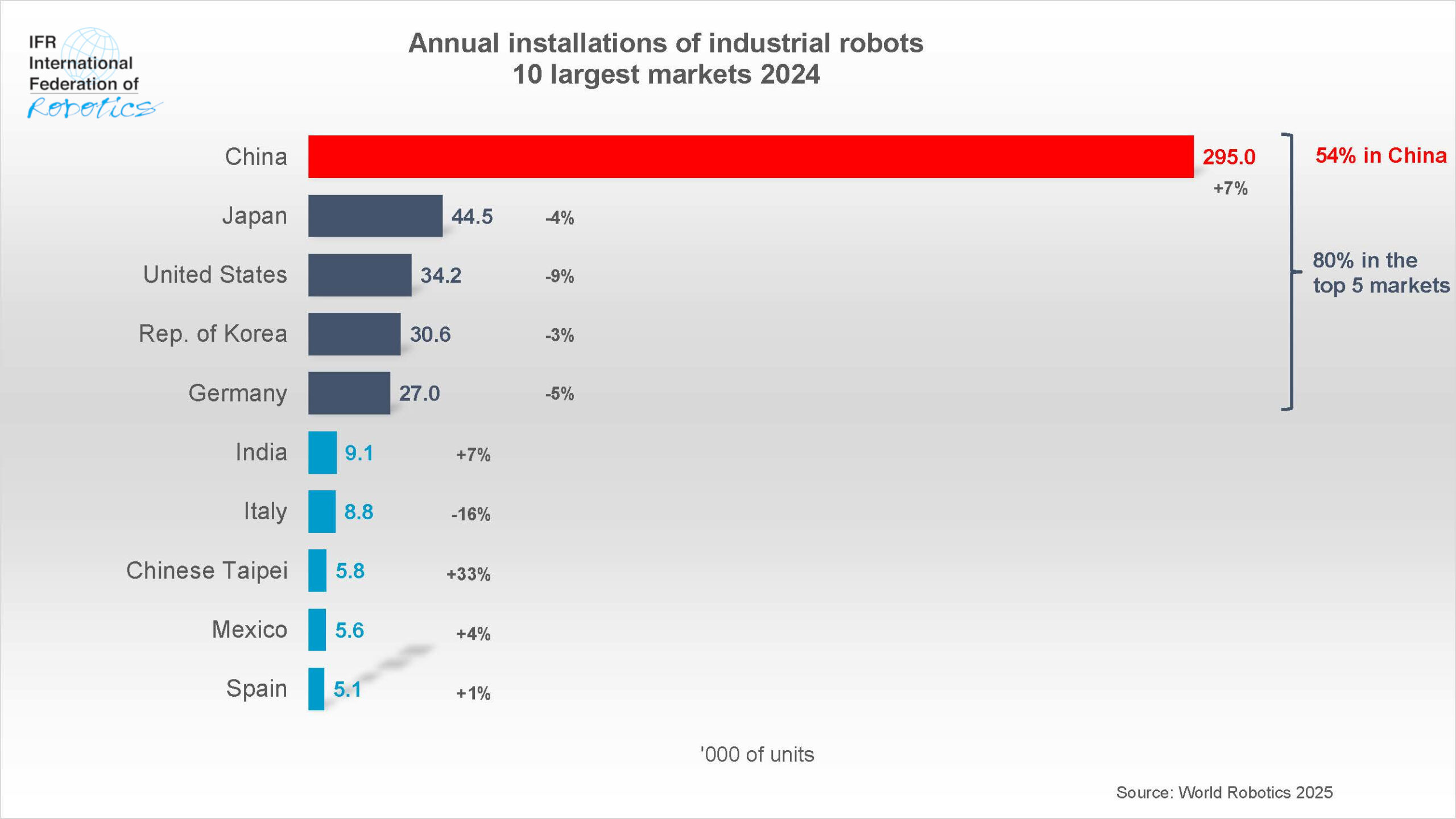

China is by far the world’s largest market in 2024, representing 54% of global deployments. The latest figures show that 295,000 industrial robots have been installed. The IFR report highlights that, for the first time, Chinese manufacturers have sold more than foreign suppliers in their home country. Their domestic market share climbed to 57% last year, up from about 28% over the past decade. Besides, China’s operational robot stock exceeded the 2 million mark in 2024.

As regards to Japan, the country maintained its position as the second-largest market for industrial robots, with 44,500 units installed in 2024. This represents a slight 4% decrease compared to the previous year. The country’s operational stock rose by 3%, with 450,500 units now in use. “Demand for robots will grow slightly by lower single-digit rates in 2025 – IFR says –. It will then accelerate to a medium single-digit rate on average in the next few years”.

The market in the Republic of Korea installed 30,600 units in 2024 – down 3%. The country is the fourth largest robot market in the world in terms of annual installations in 2024, after the United States, Japan, and China.

Finally, India continues to grow with a record of 9,100 units installed in 2024 – up 7%. In terms of annual installations, India ranks sixth worldwide, one place up behind Germany.

Robot installations in Europe fell 8% in 2024

Industrial robot installations in Europe fell 8% to 85,000 units in 2024. But this is still the second largest number recorded in history. 80% of all European robot installations took place in the European Union (67,800 units). Robot demand in Europe benefited from the nearshoring trend. The annual average growth rate from 2019 to 2024 was plus 3%.

Considering the different countries, Germany is the largest robot market in Europe and the fifth-largest in the world. Installations fell 5% to 26,982 units in 2024, which is however the second-best result recorded after the record year of 2023. This represents a 32% market share of the annual total in Europe.

The number of installations in Italy, the second largest European market, fell by 16% to 8,783 units. Spain is now in third place (5,100 units) and France (4,900 units) moved down to fourth place, with a 24% decrease.

As regards to the UK, industrial robot installations were down 35% to 2,500 units in 2024. “The record number of 3,800 units in 2023 – IFR comments – was a one-off peak, driven by the ‘super-deduction’ tax credit program, which ended after the first quarter of 2023”. Robot installations in the UK rank 19th worldwide in 2024.

The installations in the Americas again exceeded 50,000 units

Robot installations in the Americas exceeded 50,000 units for the fourth year in a row: 50,100 units were installed in 2024, down 10% below the level reached 2023.

The United States, the largest regional market, accounted for 68% of installations in the Americas in 2024. Robot installations were down by 9% to 34,200 units. The United States imports most of its robots from Japan and Europe, with few domestic suppliers. However, there are numerous domestic robot system integrators implementing robotic automation solutions.

Total installations in Mexico reached 5,600 units in 2024, a decrease of 4% compared to the previous year. And in Canada, robot installations declined by 12% to 3,800 units.

){kind=link}